COVID-19 and the Recent Market Sell-Off

The world has never experienced a disease outbreak like this one. It’s LIVE, with dramatic pictures, live data and videos. Because of this, human emotions and behaviors play a much bigger role than past outbreaks.

As I write this memo on Tuesday morning, scientists, medical professionals and government health officials around the world are working to understand how the new virus is spreading, trying to contain it, and working on a new vaccine. Unfortunately at this time, we can say that containment has failed so far.

Up until Friday, the Centers for Disease Control and Prevention (CDC) used a very limited definition for a person under investigation (“PUI”). This narrow definition limited who could be tested for COVID 19 and many potentially infected people were not even tested. There is no doubt that the virus has continued to spread. On Friday, the CDC expanded their definition after the first case of infection from an unknown origin arose.

We’re not doctors or scientists and obviously can’t advise on these issues other than telling you to listen to the professionals. However, we do understand growth functions and statistics. The growth of new cases confirms that the growth is exponential, not linear. Since January 16, when the Chinese government officially admitted they had an outbreak on their hands and started releasing numbers, new cases have been doubling every few days in different countries around the world.

The implications for the world economy may be severe as we could experience supply and demand shocks. We already see the casualties in the airline, hotel and restaurant sectors. In the next days and weeks, we will see governments and central banks take extreme measures to stop the virus from spreading and to limit the implications for the global economy.

Let’s ignore for a moment the fact that this recent drop barely qualifies as a correction. This correction has just happened at a faster pace than past corrections and its connection to the virus caused panic among investors.

Over the weekend, I heard many investment professionals say that you can’t avoid these losses and that no one could have predicted this. But managing wealth is not about knowing when a major drop in asset prices will occur (good luck with that). It’s about being prepared and building portfolios that are resilient to significant shocks.

Before I continue, I want to refer you to a memo I wrote last year, which I think is one of the most important memos I’ve ever written. It is more relevant today than the time I wrote it, especially regarding the media (both traditional and social).

Where Were We Just Before the Virus-Related Sell-Off?

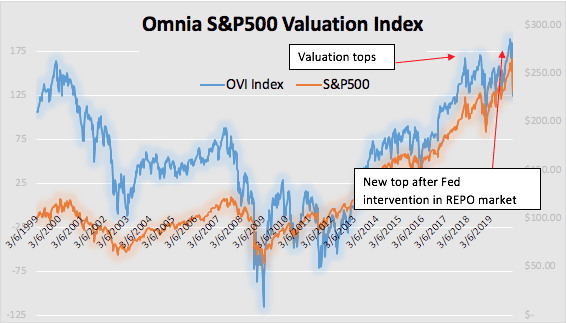

The information below will show us how vulnerable the market was to begin with and how it was potentially primed for a sharp correction due to any small reason. To state it plainly: market valuations were stretched. We pointed out several times in the past year that we didn’t like the valuations that US equities were trading at. We also said the markets could continue to go ever higher, but at extreme levels, you want to manage the increased risk. The S&P 500 dropped sharply after hitting extreme valuations (about 170 on our index) in January 2018 and in September 2018, but rebounded and broke out to even higher levels in November 2019 as the Fed once again provided stimulus through the REPO market.

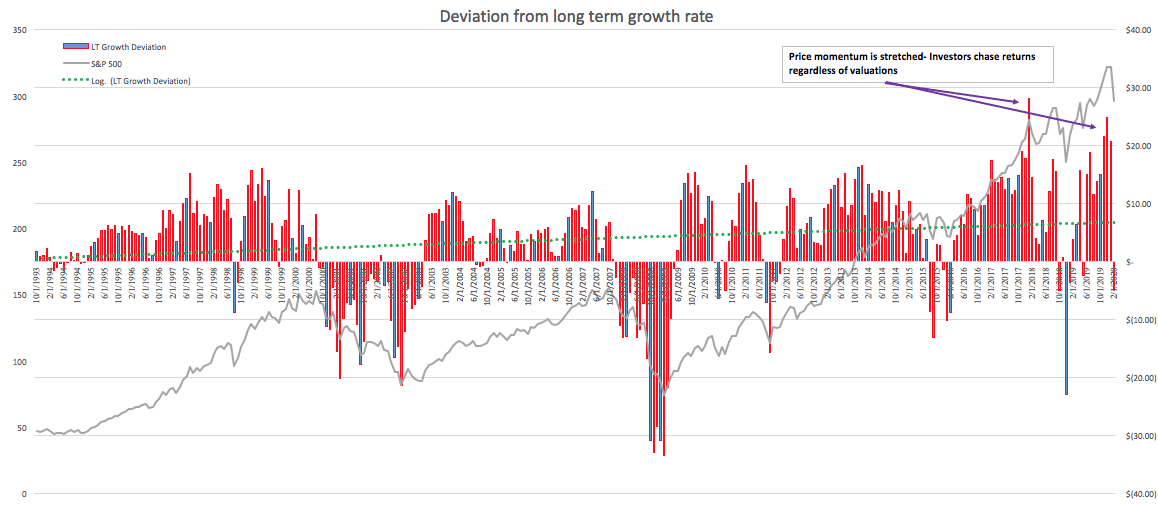

Price Momentum and Investor Optimism Were Stretched

In the chart below, you will find an index we built to identify extreme market behaviors (i.e. deviation from long-term growth rates), either positive or negative. As you can see, in December 2019 investors were extremely optimistic and were driving prices higher at an unsustainable rate. This is another indicator of risks accumulating just before the recent sell-off. By the way, this chart also shows that extreme market behaviors have become consistently more commonplace since 2008.

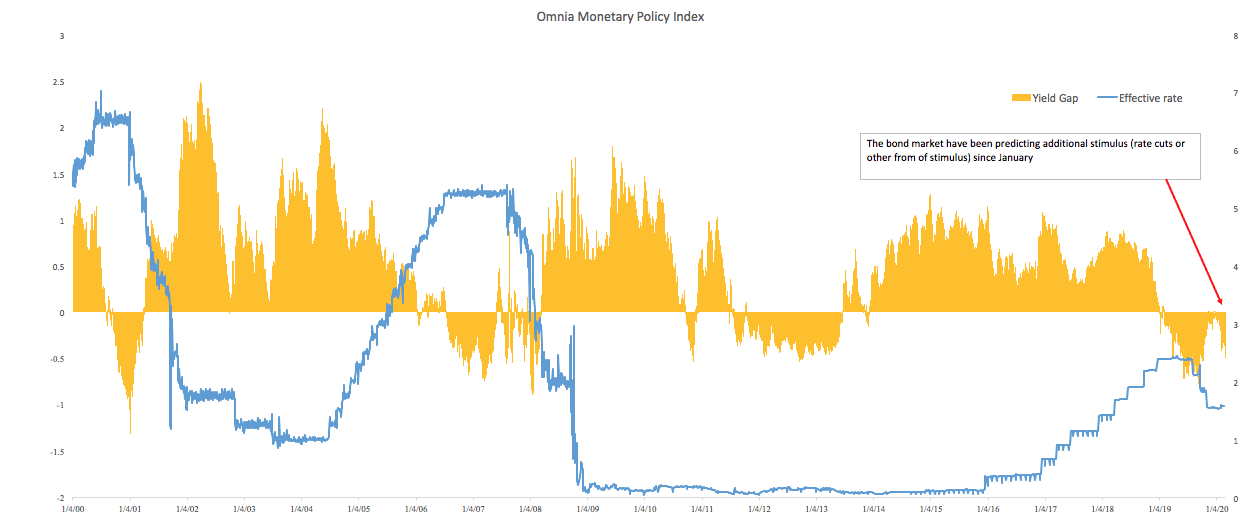

What Has the Bond Market Been Saying?

Since February 2019, the bond market has been telling us that the Fed would be forced to provide additional stimulus. Between August and October 2019, the Fed cut rates three times. After the three rate cuts, the bond market (and our index) recovered and turned positive until January 2020 when it started plunging again. As I have written in the past, the treasury market provides a tremendous amount of valuable information for investors and investors should pay attention to those signals.

Summary

The current situation is dynamic and developing by the hour. We were already concerned about equity market valuations and the fragility of the economy, and the coronavirus adds another big risk to financial markets.

An event such as this is no doubt a black swan, and by definition can’t be predicted. But you don’t need to be predictive when building your portfolio. Equity markets are prone to sharp drops and recessions are a fact of life for the economic cycle. Every portfolio needs to be built taking these facts into consideration. As we show above, you also want to have and follow a process informed by objective measures, or you leave your wealth vulnerable to randomness and uncertainty.

Click here to download the article.

Important Information

Omnia Family Wealth, LLC (“Omnia”), a multi-family office, is a registered investment advisor with the SEC. This commentary is provided for educational and informational purposes only. It does not take into account any investor’s particular investment objectives, strategies, tax status, or investment horizon. No portion of any statement included herein is to be construed as a solicitation to the rendering of personalized investment advice nor an offer to buy or sell a security through this communication. Consult with an accountant or attorney regarding individual tax or legal advice.

Advisory services are only offered to clients or prospective clients where Omnia Family Wealth and its representatives are properly licensed or exempt from licensure. Information in this message is for the intended recipient[s] only. Please visit our website https://omniawealth.com for important disclosures.

This content is provided for informational purposes only and is not intended as a recommendation to invest in any particular asset class or strategy or as a promise of future performance. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve.

The views expressed herein are the view of Omnia only through the date of this report and are subject to change based on market or other conditions. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. Omnia has not conducted an independent verification of the data. The information herein may include inaccuracies or typographical errors. Due to various factors, including the inherent possibility of human or mechanical error, the accuracy, completeness, timeliness and correct sequencing of such information and the results obtained from its use are not guaranteed by Omnia. No representation, warranty, or undertaking, express or implied, is given as to the accuracy or completeness of the information or opinions contained in this report. This report is not an advertisement. It is being distributed for informational and discussion purposes only. Omnia shall not be responsible for investment decisions, damages, or other losses resulting from the use of the information. This report is not intended for public use or distribution. The information contained herein is confidential commercial or financial information, the disclosure of which would cause substantial competitive harm to you, Omnia, or the person or entity from whom the information was obtained, and may not be disclosed except as required by applicable law.

Statements that are non-factual in nature, including opinions, projections, and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Further, all information, including opinions and facts expressed herein are current as of the date appearing in this report and is subject to change without notice. Unless otherwise indicated, dates indicated by the name of a month and a year are the end of the month.

Have Questions for An Advisor?

RELATED ARTICLES

THE CATCH-22 OF INVESTING IN ARTIFICIAL INTELLIGENCE

Read More

PRIVATE CREDIT: DATA, DISCIPLINE, AND DIVERSIFICATION

Read More

IT’S TIME FOR HEALTH CARE TO PUT BRAIN HEALTH FRONT AND CENTER

Read More

PRIVATE CREDIT: OPPORTUNITY AND THE CRITICAL ROLE OF MANAGER SELECTION

Read More

BEYOND THE HEADLINES: HOW GEOPOLITICS MOVES MARKETS

Read More

TRUMP’S TARIFF STRATEGY: A Comprehensive Overview

Read More

The Exit Trap: Avoiding the Illusion of Forever Wealth

Read More