DEFENSE TECH: THE CONVERGENCE CYCLE

By: Alon Ozer & Lawrence Muscant

FROM OUR MEMO TO INVESTORS, APRIL 2020

We believe we will see a fiscal stimulus of closer to $5 trillion if not more. The budget deficit isn’t playing a role in such a situation (the problem should have been addressed years ago) and the debt-to-GDP ratio will surpass the last record we had during WWII. As part of the fiscal policy, the U.S. needs to invest trillions of dollars in new technologies, compensating for years of under-investment. When the Soviet Union launched the world’s first satellite in 1957, the U.S. response was creating NASA in 1958. Today we should act the same and invest in quantum computing, artificial intelligence, biotech, nanotech, agriculture technologies, green energy, and robotics. The government can fund new initiatives like the successful Yozma public-private partnership program that Israel created in the early 1990s to generate billions of extra tax revenues and profits for investors. This is also the only realistic solution to fix our deficit problems in the long run: We need to invest in producing technologies that will improve Americans’ lives and keep America a leading technology power. Defense and AI have already converged. But the deeper transformation underway is broader than either sector alone. Economic security, energy security, AI infrastructure, industrial policy, and national security are increasingly becoming different expressions of the same global capital cycle.

Since writing that memo to clients right after COVID, our firm has not just been observing this transition, we have been actively building positions and deploying capital into the deep-tech space. Across venture and growth-stage investments, public-market expressions, and specialty credit, our team has spent the last six years building underwriting expertise in the technologies and structures that sit at the intersection of defense, AI, energy, and industrial policy. What follows is an updated framework with a sharper defense-tech focus, calibrated to what has actually happened since, and a current map of where the asymmetry now sits and how to access it.

EXECUTIVE SUMMARY

Six years on, the thesis has materialized faster than we expected. Defense and technology are now collapsing into a single capital cycle, organized around national security, compute, energy, and supply-chain control. The U.S. State Department’s Pax Silica framework, launched in December 2025, gives the convergence a formal policy architecture.¹ The U.S.-Israeli campaign against Iran provided its operational validation. The European deep-tech VC market has emerged as a meaningful pipeline. The hyperscaler capex cycle is its compute backbone.

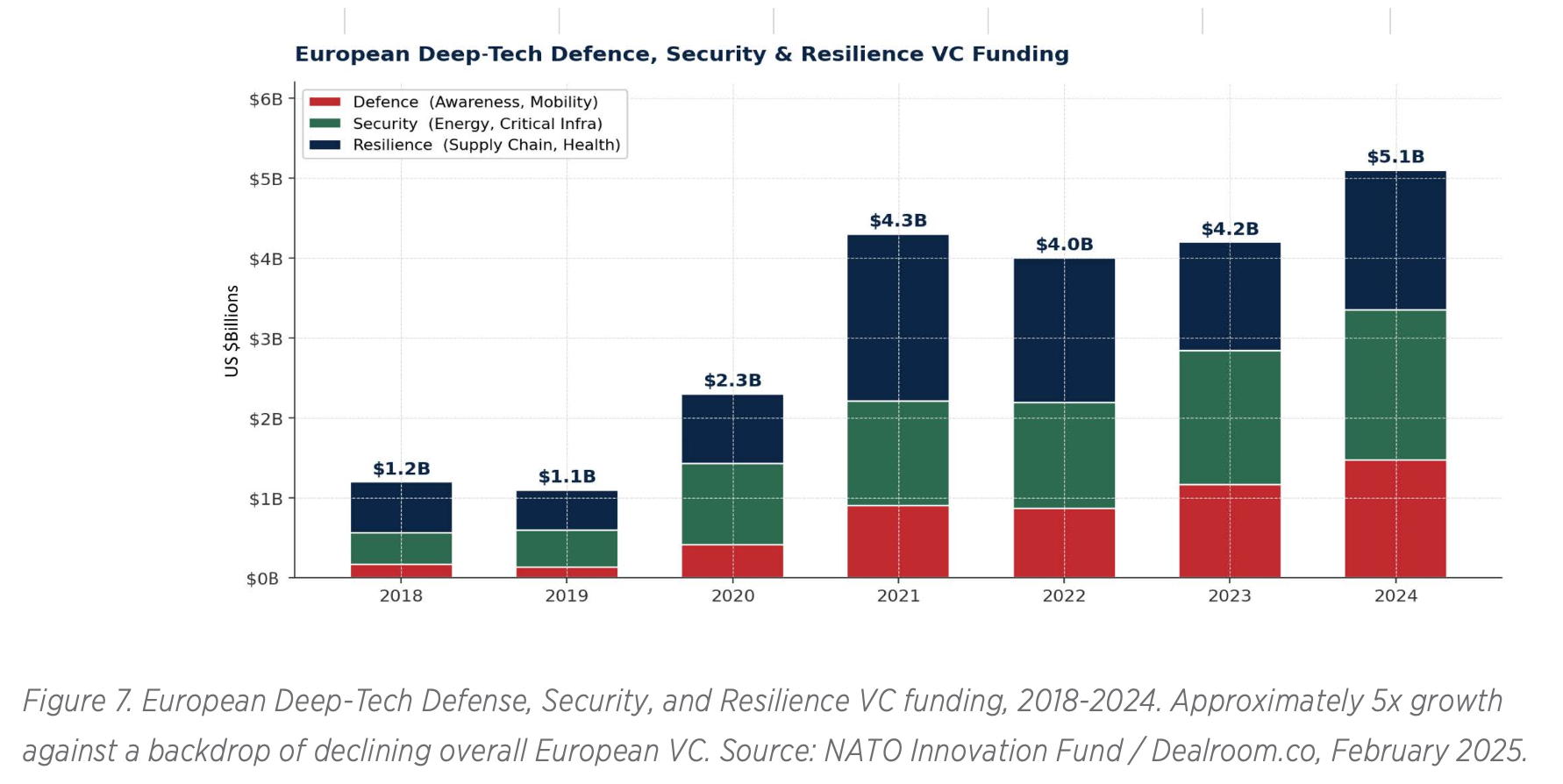

The investable surface area is wider than the obvious primes. The asymmetry sits in three places: the second-order physical infrastructure layer that must scale alongside AI compute (what we call Physical AI), the European deep-tech ecosystem where defense, security, and resilience VC funding has grown 5x in six years to $5.2B in 2024², and the Israeli defense-technology base whose battle-tested capabilities remain, in many respects, unmatched and are now formally integrated with U.S. industrial policy through the bilateral Strategic Partnership on AI signed in January 2026.³

PART I | THE RETURN OF ECONOMIC STATECRAFT

For most of the post-Cold War era, markets operated under the assumption that efficiency mattered more than resilience, globalization mattered more than industrial policy, and private capital allocation mattered more than state strategy. That era is ending. Governments are now actively shaping energy systems, semiconductor supply chains, critical- minerals access, AI infrastructure, and communications architecture as matters of strategic national interest.

The Foundation for Defense of Democracies’ recent Gameplan for American Economic Security captures the shift: adversarial states now treat markets, supply chains, finance, and critical infrastructure as strategic battlefields.4 The implication is that government policy is no longer simply a backdrop to markets. It is becoming an active force shaping capital flows, industrial priorities, and valuation premiums across strategic sectors.

Two recent conflicts have crystallized the new framing. Ukraine demonstrated that modern warfare still consumes enormous industrial output, and also that drones, surveillance systems, electronic warfare, and AI-enabled targeting are decisive. NATO has struggled to replenish depleted stockpiles. The U.S.-Israeli campaign against Iran has been more prolonged than initially expected and has stress-tested Western air-dominance doctrine. The conclusion governments are drawing is consistent: structurally higher defense spending, stronger domestic industrial capacity, and more advanced military technologies, not for one year, but for the foreseeable future.

PART II | SIZING THE SPEND

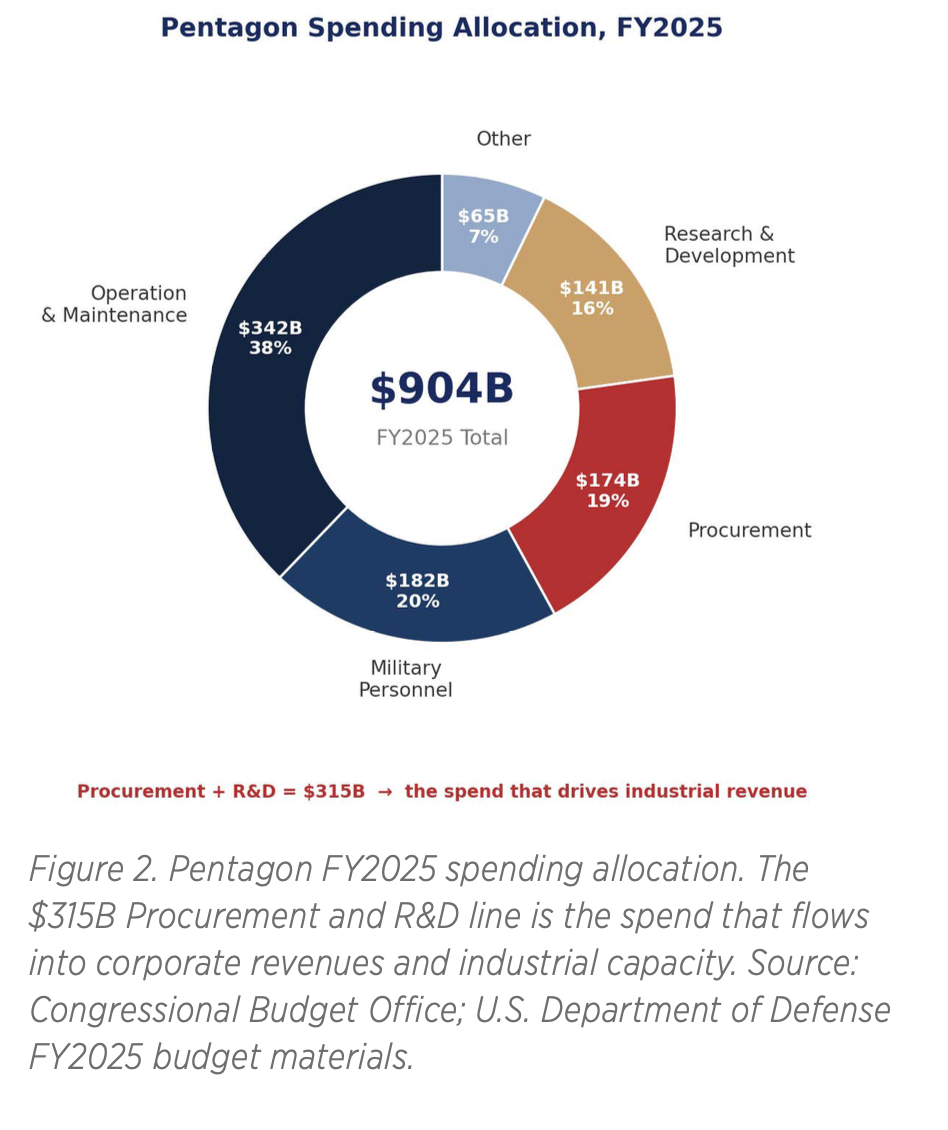

The United States spent $954 billion on defense in 2025, down 7.5% in real terms from $997 billion in 2024, primarily reflecting the cessation of new Ukraine aid appropriations during the year.5 The U.S. remains far and away the world’s largest military spender, but at roughly 3% of GDP, the spending is historically low as a share of the economy, well below the reference points of 10% during the Vietnam War and 7% at the peak of the Cold War. There is meaningful room to expand. The administration has formally requested $1.5 trillion in defense spending for FY2027, a 44% increase over total FY2026 defense fund ing of approximately $1.05 trillion (announced January 8, 2026; formal request submitted April 2026).6

The United States spent $954 billion on defense in 2025, down 7.5% in real terms from $997 billion in 2024, primarily reflecting the cessation of new Ukraine aid appropriations during the year.5 The U.S. remains far and away the world’s largest military spender, but at roughly 3% of GDP, the spending is historically low as a share of the economy, well below the reference points of 10% during the Vietnam War and 7% at the peak of the Cold War. There is meaningful room to expand. The administration has formally requested $1.5 trillion in defense spending for FY2027, a 44% increase over total FY2026 defense fund ing of approximately $1.05 trillion (announced January 8, 2026; formal request submitted April 2026).6

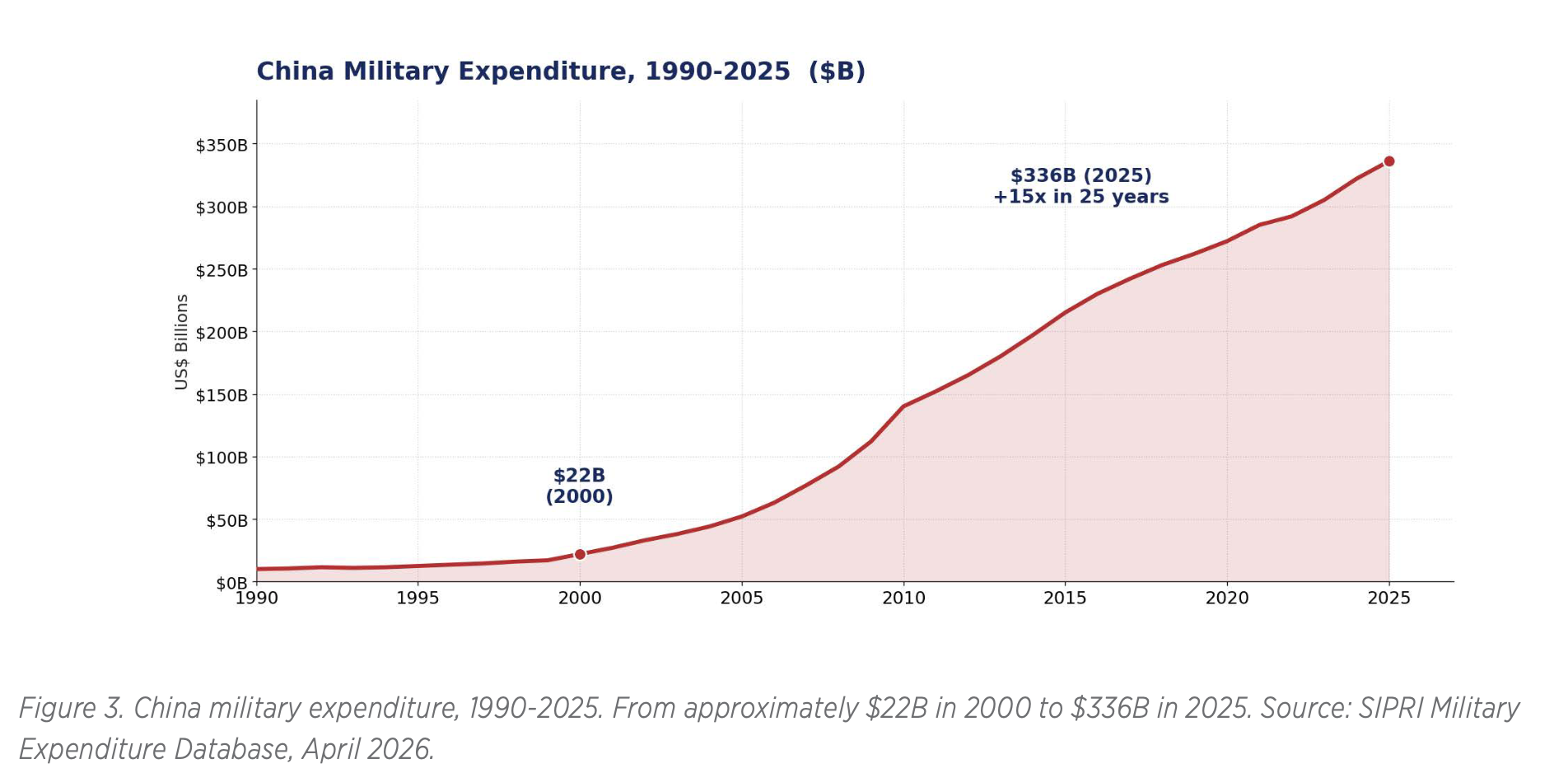

The forcing function is China. Chinese military spending grew 7.4% in real terms in 2025 to $336 billion, the 31st consecutive year-on- year increase and roughly fifteen times its $22 billion level in 2000.7 U.S. policymakers no longer view supply-chain dependence on adversaries as a benign cost-optimization story. The reframing is what makes industrial policy bipartisan and durable.

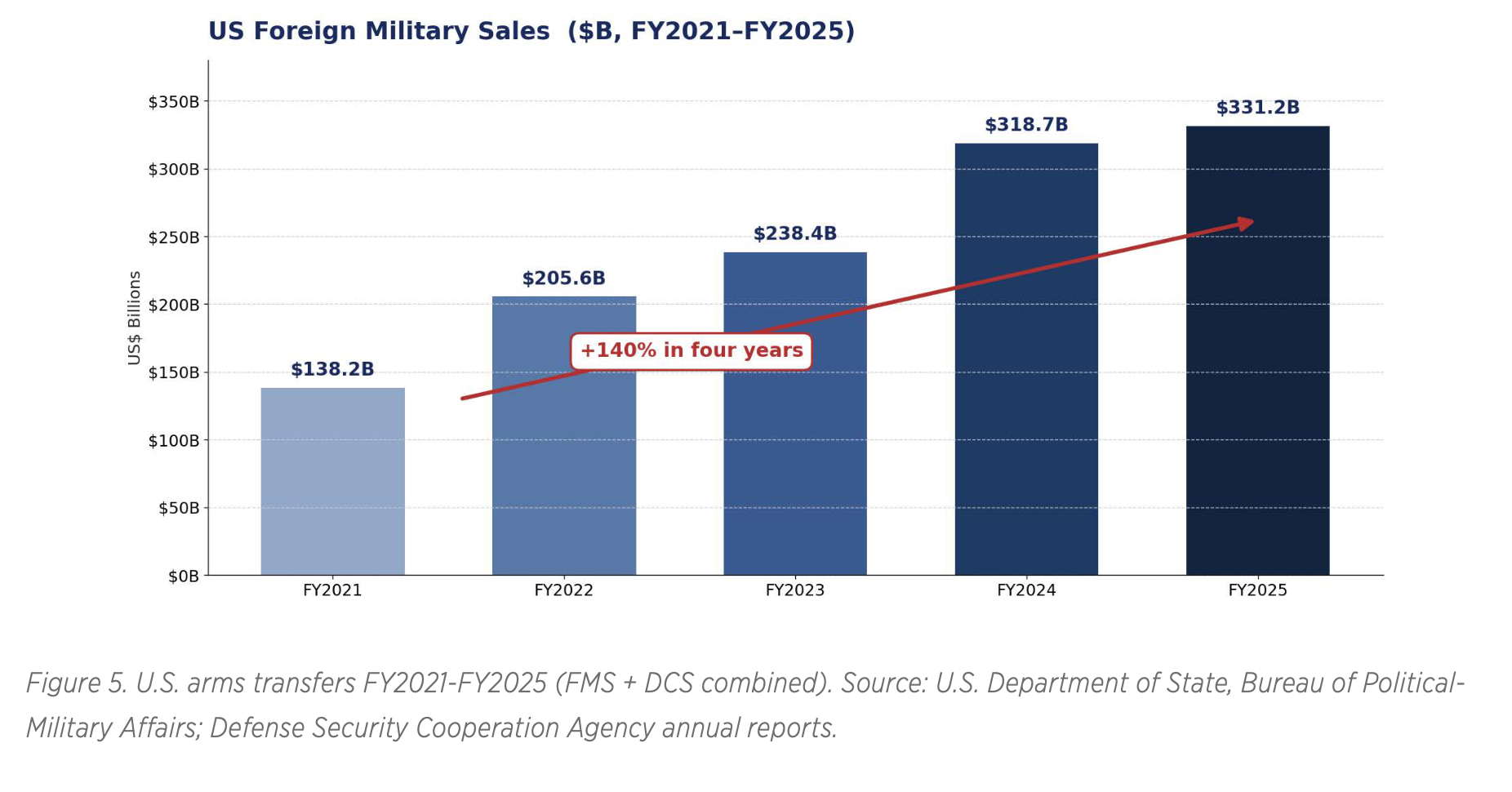

Foreign demand for American military equipment more than doubled in four years, from $138 billion in FY2021 to $331 billion in FY2025. The FY2025 total combined $104.4 billion in government-to-government Foreign Military Sales (FMS) and $226.8 billion in private-sector Direct Commercial Sales (DCS), the highest DCS figure on record.8 Arms sales convert to contract revenue and deliveries with a multi-year lag, so this is a leading indicator of revenue that has not yet flowed through to the primes.

PART III | PAX SILICA AND THE TRUSTED-COUNTRY PREMIUM

The most important policy development for understanding capital flows in this cycle has received remarkably little attention from public-markets investors. In December 2025, the U.S. State Department launched Pax Silica, its flagship framework on AI and supply-chain security.9 The framing in the founding declaration is direct: if the 20th century ran on oil and steel, the 21st century runs on compute and the minerals that feed it.

Pax Silica is a coordinated economic and industrial-policy framework binding the United States to a defined set of trusted partners: Australia, Greece, India, Israel, Japan, Republic of Korea, Singapore, United Arab Emirates, and the United Kingdom, with Taiwan endorsing the principles through a separate joint statement. The signatory geography is not random. It is a deliberate selection of economies combining advanced semiconductor capability, critical-mineral reserves, capital and demand, industrial-base capacity, and frontier defense technology.

For investors, the structural implication is what we are calling a “trusted-country premium.” Companies operating within Pax Silica signatory geographies have a different risk profile than those exposed to coercive-dependency jurisdictions. Capital allocation into the AI and defense-tech complex now has a formal trusted-counterparty framework, which will reshape how multinationals build supply chains, where venture capital deploys, and which equities the market is willing to underwrite at premium multiples.

PART IV | PHYSICAL AI: THE BOTTLENECK LAYER

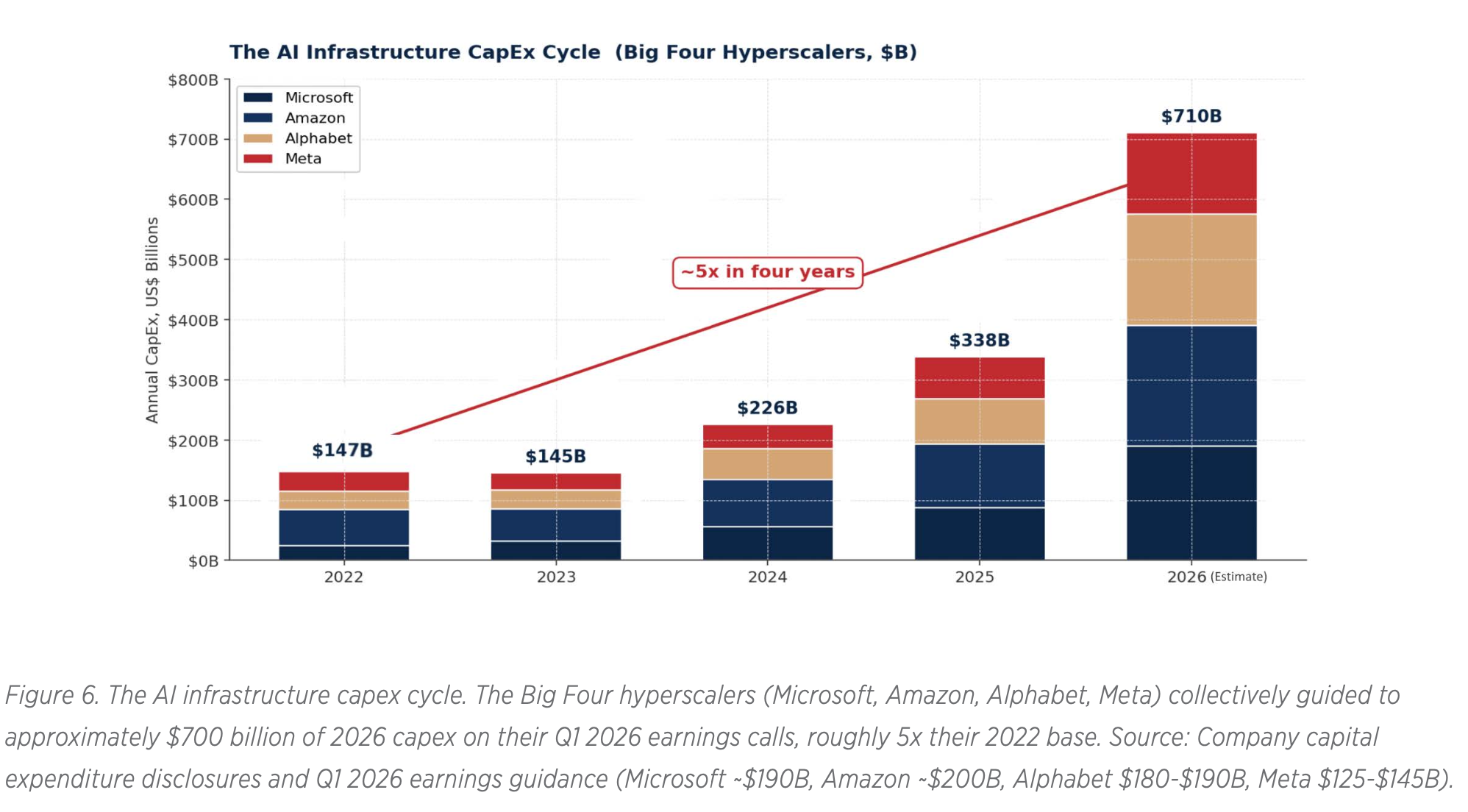

Sophisticated investors understand that AI isn’t just a software revolution, it is becoming a physical infrastructure revolution. The bottleneck is shifting from algorithms to physical capacity. Commercializing AI at scale requires enormous investments in electricity generation, transmission, semiconductors, cooling, data centers, fiber, and secure compute. Compute itself is now both an economic input and a strategic asset.

The scarce resource is no longer software talent or even semiconductor supply. It is power itself. The U.S. National Energy Dominance Council, established by Executive Order 14213 on February 14, 2025, reflects Washington’s recognition that AI leadership, industrial competitiveness, and geopolitical influence increasingly depend on abundant, reliable, and domestically controlled energy infrastructure.10 The race for AI leadership is simultaneously a race for power generation capacity.

Three operative bottlenecks deserve emphasis. First, semiconductors as national security: Taiwan still produces more than 90% of the world’s most advanced chips,11 and Pax Silica’s semiconductor pillar is the policy response. Second, AI as a dual-use capital cycle: the same capabilities driving enterprise productivity are driving autonomous weapons, electronic warfare, and decision-support systems. There is no clean line to draw between civilian and military compute. Third, power and infrastructure: the market has spent two years pricing AI through software and semiconductors and has been slower to price the physical layer that must scale alongside them. That is where the asymmetry currently lives.

PART V | THE EUROPEAN THEATRE

European deep-tech defense, security, and resilience is the fastest-growing major venture capital category in Europe. While European total VC funding declined approximately 45% from peak over 2022-2024, the DSR sub-sector grew over 30%.12 In 2024 it reached an all-time high of $5.2 billion, roughly 5x its 2018 base, and now represents approximately 10% of all European VC funding and one-third of all European deep-tech funding.

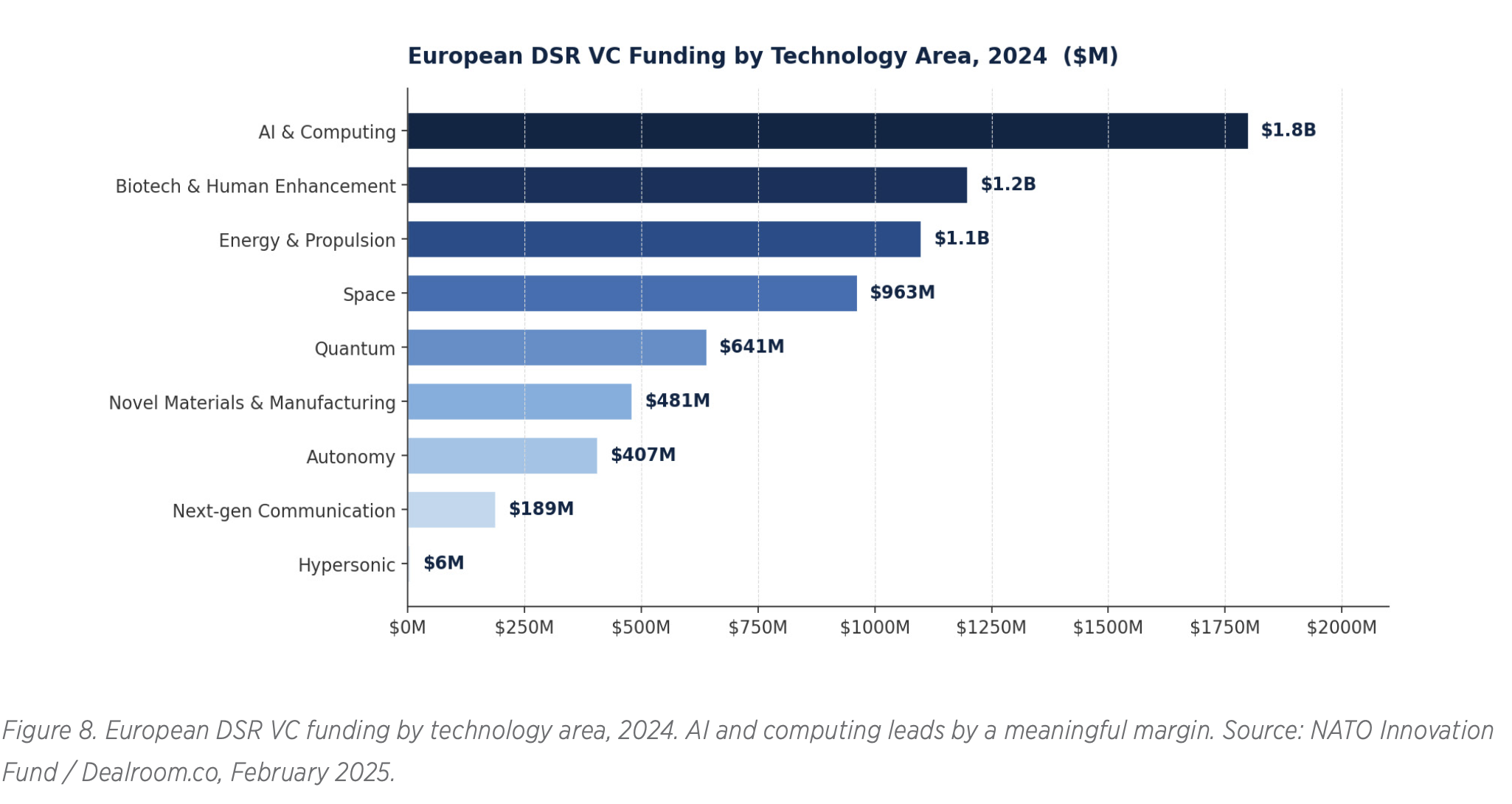

AI and computing have emerged as the dominant technology category within European DSR, attracting $1.8 billion in 2024 alone. Biotech and human enhancement, energy and propulsion, space, and quantum follow as the major investment areas. Geographically, the UK has attracted the most cumulative funding since 2019 ($7.1B), Germany the most in 2024 ($1.3B), and Munich has emerged as Europe’s leading single hub for defense-tech venture capital. Switzerland and the Netherlands have the highest share of total VC going to DSR, at over 7%.

M&A in European defense tech is accelerating as European primes and U.S. strategic acquirers absorb the most operationally relevant venture-backed companies. The IPO window remains closed since 2021, but private-market liquidity through trade- sale exits is improving meaningfully. Three observations are worth carrying. First, the growth rate of European DSR funding is substantially faster than the broader European venture market, indicating capital rotation toward the theme rather than just a rising tide. Second, the U.S. share of European DSR funding has been approximately 25% in 2024, meaning capital is flowing trans-Atlantically in both directions. Third, the European deep-tech ecosystem is relatively unconsolidated compared to U.S. defense tech, with a wider distribution of investable companies at earlier stages but also greater dispersion in outcomes.

PART VI | ISRAEL: THE UNMATCHED EDGE

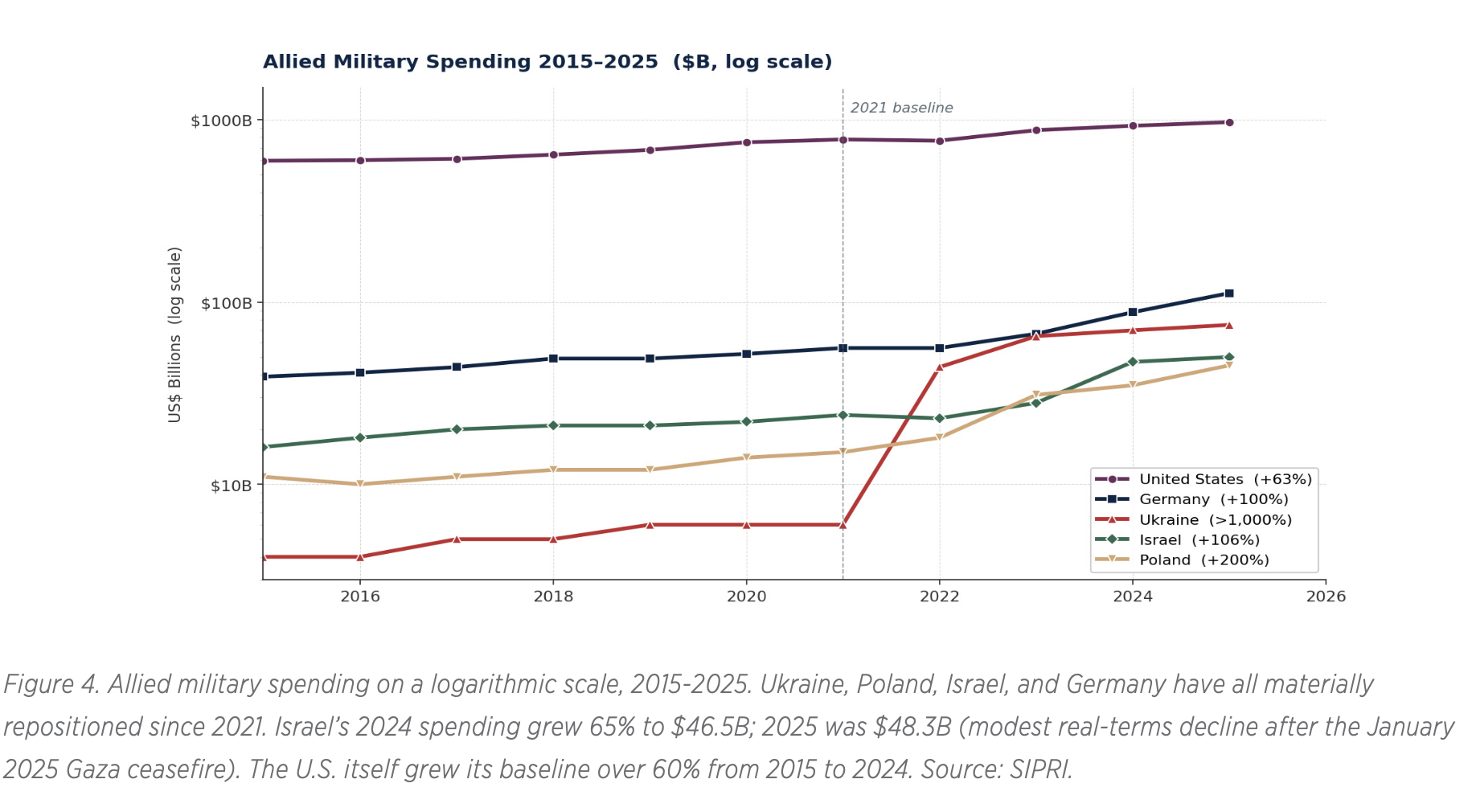

Israel occupies a unique position in the global defense-technology ecosystem, and the U.S.-Israeli campaign against Iran has substantially widened the gap between what this defense technology can do operationally and what the rest of the world fully understands about how it does it. Israeli military spending peaked at $46.5 billion in 2024 (a 65% real-terms increase, the largest single-year jump since the Six-Day War in 1967) and was $48.3 billion in 2025, declining 4.9% in real terms after the January 2025 Gaza ceasefire.13 Israeli military spending remains 97% higher than 2022 levels.

WHAT WAS DEMONSTRATED

The publicly visible elements of the U.S.-Israeli campaign against Iran represent the most extensive operational test of advanced military technology since the Gulf War. The demonstrated capabilities include: multi-tier integrated air defense at scale (Iron Dome, David’s Sling, Arrow 3, and Arrow 4 functioning as an integrated system against a sustained, multi-vector missile and drone attack from extreme range; no other nation has operationally validated a comparable architecture); long-range precision strike against hardened, deeply buried facilities; suppression of Iranian S-300 and indigenous Bavar-373 air defenses via what appear to be advanced electronic-warfare or cyber capabilities; AI-fused real-time targeting at machine speed; and parallel cyber operations of unknown scale.

WHAT REMAINS OPAQUE

For most major weapons systems used by the U.S. or European militaries, the broad technical envelope is publicly understood. For a meaningful subset of the U.S.-Israeli capabilities demonstrated against Iran, the public record reveals only fragments. The actual interception rates of Arrow 3 and Arrow 4 against the specific Iranian threat set have not been published. The architecture of the AI/ML systems used for sensor fusion and dynamic targeting has not been publicly described, but the operational tempo implies a maturity beyond any publicly known equivalent. The munitions used against deeply buried hardened targets have not been identified, and several capabilities consistent with what was observed are not known to be in standard U.S. or NATO inventories. The specific electronic-warfare and cyber capabilities deployed to neutralize Iranian air defenses remain classified.

This opacity is itself a structural feature of the Israeli defense ecosystem and a form of strategic moat. The U.S.-Israeli campaign against Iran deepened the moat by demonstrating outcomes without revealing methods.

THE ALLIANCE AND THE INVESTMENT IMPLICATION

On January 16, 2026, the United States and Israel signed a Strategic Partnership on Artificial Intelligence, Research, and Critical Technologies, one of the earliest formal bilateral integrations under Pax Silica.14 The agreement covers AI research and development, advanced computing infrastructure, quantum, novel materials, hypersonic systems, and energy and propulsion. It complements the long-standing BIRD and BIRD-Defense frameworks that have been funding U.S.-Israeli joint R&D for decades.

The alliance is structurally important for three reasons. Operational validation: Israel is the only U.S. ally that has run a sustained, modern, high-tempo combat operation against an adversary with comparable technological inventory, and the capability data generated is uniquely valuable to U.S. force planning. Talent and ecosystem depth: Israel produces a disproportionate share of the world’s elite military-technical talent, with structurally embedded dual-use transfer into civilian AI, cyber, and deep- tech. Geographic positioning: the Pax Silica signatory geography is heavily weighted toward Indo-Pacific partners, and Israel is the primary Western anchor in the Middle East. For investors, the public-market expressions and the broader growth-stage Israeli defense-tech ecosystem are both structurally attractive entry points; access typically requires either local presence or relationships with Israeli venture managers focused on the sector.

CLOSING

Defense is no longer a sector. AI is no longer a sector. They are facets of the same capital cycle, one driven by a structural reordering of the global economy around national security, technological supremacy, and supply-chain resilience. Pax Silica is its policy crystallization. The U.S.-Israeli demonstration against Iran is its operational validation. European deep- tech VC is its early-stage funding pipeline. The hyperscaler capex cycle is its compute backbone.

The useful question we keep asking of any position in this complex is not whether it is “defense” or “AI.” It is whether the position is exposed to the convergence, the place where the two cycles overlap and where the market is still pricing two separate stories instead of one. That is where the asymmetry sits, and that is where we are continuing to concentrate our work.

SOURCES

- 1.U.S. State Department

- 2.NATO Innovation Fund / Dealroom.co, February 2025

- 3.U.S. State Department joint statement, January 16, 2026

- 4.FDD, 2025

- 5.SIPRI April 2026

- 6.White House / Office of Management and Budget; Foundation for Defense of Democracies analysis

- 7.SIPRI April 2026

- 8.U.S. Department of State, Bureau of Political-Military Affairs, March 2026 release

- 9.U.S. State Department

- 10.Executive Order 14213; U.S. Department of Energy

- 11.TrendForce; BCG semiconductor industry analyses

- 12.NATO Innovation Fund / Dealroom.co, February 2025

- 13.SIPRI

- 14.U.S. State Department joint statement

IMPORTANT INFORMATION

Omnia Family Wealth, LLC (“Omnia Family Wealth”) is a registered investment advisor with the SEC. Advisory services are only offered to clients or prospective clients where Omnia Family Wealth and its representatives are properly licensed or exempt from licensure.

The information provided is for educational and informational purposes only and does not constitute investment advice and it should not be relied on as such. It should not be considered a solicitation to buy or an offer to sell a security. It does not take into account any investor’s particular investment objectives, strategies, tax status or investment horizon. You should consult your attorney or tax advisor.

The views expressed in this commentary are subject to change based on market and other conditions. These documents may contain certain statements that may be deemed forward looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those projected. Any projections, market outlooks, or estimates are based upon certain assumptions and should not be construed as indicative of actual events that will occur.

All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such.

For additional information, please visit our website at www.omniawealth.com. For current Omnia Family Wealth information, please visit the Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov by searching with Omnia Family Wealth’s CRD #170909.

Have Questions for An Advisor?

RELATED ARTICLES

Omnia Family Wealth’s Michael Wagner Featured in MSN

Read More

Omnia Family Wealth’s Michael Wagner Featured on CNBC

Read More

Omnia Family Wealth’s Michael Wagner Featured in Barron’s

Read More

Omnia Family Wealth’s Lawrence Muscant Explores Geopolitical Forces Shaping Capital Markets

Read More

Grateful for Ten Years Together

Read More

Omnia Family Wealth Named to Financial Advisor Magazine’s 2025 Top RIA List

Read More

Michael Wagner Featured in MarketWatch: Reading Forecasts Without Being Misled

Read More